2.1.18

Feeling confident: Steps to saving more

In 2016, 21% of U.S. workers said they were very confident they would have enough money for a comfortable retirement. This was about the same percentage as in 2015, but both years showed a big increase in confidence from the 13% level in 2013, when many Americans were still struggling to recover from the Great Recession.1

When it comes to your own retirement, of course, trends don’t really matter. The question is, do you feel very confident that you will have enough money to enjoy the kind of retirement you envision? Even if you do, it’s smart to save more, and it may not be as difficult as you think.

Take the Match

If you participate in a workplace retirement plan such as a 401(k), 403(b), or 457 plan, you can choose to contribute a specific percentage of your salary, up to annual contribution limits. That’s why they are formally called defined-contribution plans. More than half of workplace plans automatically enroll new workers at a 4% rate.2 However, a common guideline suggests that workers should save about 15% of their salaries, and you may need to save more if you get a late start.

One of the best ways to boost your savings is to take advantage of any matching funds offered by your employer. For example, if your employer will match 50% of your contributions up to 6% of your salary, saving 6% on your part would result in saving 9% of your salary (6% from you and 3% from your employer).

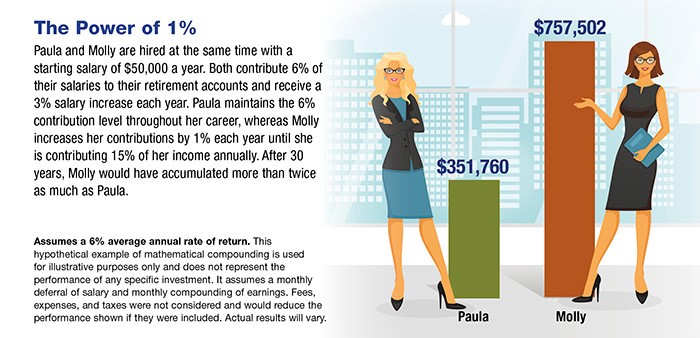

Increase by Increments

How can you save even more? You might try increasing your contributions by 1% each year. Some employers may increase your contributions automatically (unless you opt out), but you can choose to do so on your own, whether you participate in a plan or save outside of the workplace. A 1% increase may not sound like much, but it could make a big difference over the course of your career (see chart).

Here are three other ways to save without making a big sacrifice in your cash flow.

Save your raise. When you receive a raise, it’s tempting to increase your spending, but this is a great opportunity to boost your retirement savings by diverting a portion of the raise into your retirement account. And when you contribute on a pre-tax basis, the difference in your take-home pay may not be significant.

Make payments toward your future. If you pay off the balance on a car loan, student loan, or credit card, consider making the same monthly payments directly to your retirement account. Because the payment is already part of your monthly budget, you could increase your savings without reducing the amount available for other expenses.

Limit the treats. You deserve an occasional reward, but spending on “little things” can add up over time. For example, if you stop for a $4 latte each day on your way to work and have another one in the afternoon, you would spend about $175 each month. If the same amount was instead invested monthly in an account earning a 6% annual return, you could accumulate more than $100,000 after 25 years.3

1) Employee Benefit Research Institute, 2016

2) Aon, 2016

3) This hypothetical example is used for illustrative purposes only and does not represent the performance of any specific investment. Fees, expenses, and taxes are not considered and would reduce the performance described if they were included. Actual results will vary.

If you’d like to take a different approach to investment planning and management, you can meet with one of our CFS* financial advisors. We will review your finances at not cost or obligation, explain your investment options, and help you find the right products for your needs. For your complimentary consultation, please schedule an appointment with a CFS* Financial Advisor at Consumers Credit Union by calling Micki at 269.488.1776. The investment services team can provide strategies to help fit your ever-changing needs.

The information in this article is not intended as tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. Copyright 2016 Emerald Connect, LLC.

* Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA/SIPC) and Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. Consumers Credit Union has contracted with CFS to make non-deposit investment products and services available to credit union members.