1.18.21

Credit score tips for home buyers

Consumers home loans

We’d love to help you with a mortgage or home equity line of credit.

Learn moreIf you’re getting ready to buy a house, get your credit score as high as possible in order to get the best rates.

When you apply for a mortgage, one of the first things a lender looks at is your credit score. The higher your score, typically the lower your interest rate. Over the life of a home loan, this can mean saving tens of thousands of dollars. So, it makes sense to get your credit score as high as possible. Use these tips for getting your credit into shape before you seek a mortgage.

Request your credit report

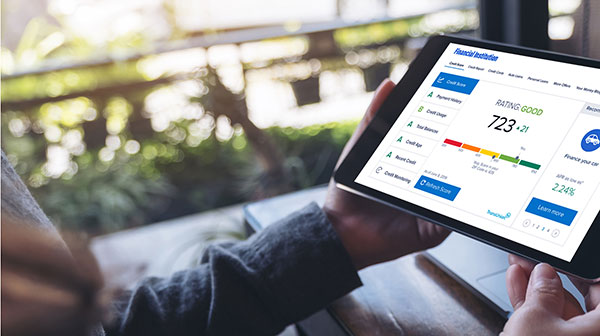

One great feature of Consumers’ Online Banking is the ability to check your credit right in your dashboard. Simply log in for instant access to your credit score and report, along with personalized tips on how to improve your score or maintain an already great one.

Additionally, records of your payment history on credit cards, loans, and other bills are tracked by three major credit bureaus— Equifax, Experian, and TransUnion—that compile reports on your creditworthiness. While most information on file is correct, sometimes it’s not due to errors or even fraud. Check what’s in your file by getting free copies of your reports at annualcreditreport.com.

You’re entitled to a free report each year from each of the credit reporting bureaus. Some people request a report from a different bureau every four months so they can keep an eye on their credit all year long.

Review your credit report and dispute any errors

When you receive your credit report(s), go over each item for accuracy. If you see any errors or accounts that aren’t yours, notify the credit bureau(s) by filing a dispute online. Here’s a sample letter for disputing credit report errors.

If you are viewing your credit report in Online Banking, there’s a button to begin a dispute right in the feature.

Avoid taking on new debt or closing old accounts

For at least six months before you plan to apply for mortgage, avoid opening lines of credit (like credit cards or car loans). Also, don’t close older accounts because they add points to your credit score.

Even after you’ve applied for a mortgage but haven’t yet finalized the deal, you should avoid opening new lines of credit or making large purchases. Lenders check your credit just before a home closes. New debt could affect your loan eligibility.

Keep current on all accounts

Paying bills on time every time will help increase your credit score.

If you have a hard time keeping track of payment schedules, consider autopay options, recurring transfers or putting alerts in your calendar to remind you of due dates.

A large, unexpected expense such as a medical bill can put a big strain on your budget and any late payments reported to the credit bureaus will ding your credit score. If you can’t pay the whole amount, call the creditor and request to make a payment plan over time. Most medical offices and hospital will work with you. When they know you have a plan to pay the bill (and you make the payments as promised), you’ll avoid having a past due account on your credit report.

Trim credit card debt

Pay down as much as you can on credit card balances and avoid making large purchases on credit. Your credit score will increase if your record shows you’re using less of your available credit. The reporting agencies call this your credit utilization rate, and it can account for up to 30% of your credit score.

We’re here to help

Our loan officers are here to help you every step of the way in getting a home mortgage. Explore your loan options online or call us at 800-991-2221.

Consumers helps more than 2,000 members finance land, first and second homes, and home improvement projects each year. We’d love to help you with a mortgage or home equity line of credit; contact us online or call us at 800-991-2221.

![]()

Consumers home loans

We’d love to help you with a mortgage or home equity line of credit.

Learn more