6.6.19

Trusts offer more than estate tax protection

The 2017 tax reform law effectively doubled the federal estate tax exclusion amount to $11.18 million for individuals who died in 2018 ($11.4 million in 2019). With the portability provision that allows the unused exclusion amount to pass to a surviving spouse, a married couple could shelter up to $22.8 million in 2019.

Trusts have often been used to help avoid estate taxes, but at these exclusion levels it’s unlikely that many families need a trust for this purpose. However, some states have estate taxes or inheritance taxes with lower exclusion amounts, and the federal amount is scheduled to revert to its pre-2018 level in 2026 unless Congress takes further action.

Even if the value of your estate seems modest, a properly constructed trust can offer many benefits, such as sparing your heirs the costly and time-consuming probate process, serving a variety of special purposes, and protecting your assets so they will be distributed according to your wishes.

Legal Control of Assets

A trust is a legal arrangement under which one person or institution controls property given by another person for the benefit of a third party. The person giving the property is referred to as the trustor (or grantor), the person controlling the property is the trustee, and the person for whom the trust operates is the beneficiary. With some trusts, you can name yourself as the trustor, the trustee, and the beneficiary.

Although you may be hesitant to give up control of your assets, in some cases it may be helpful to choose an independent trustee who would be subject to strict legal requirements in administering the trust.

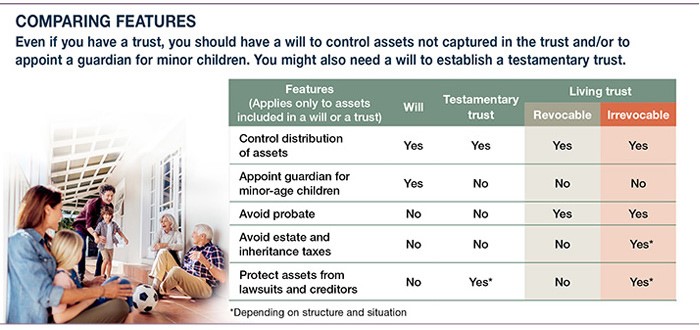

Testamentary vs. Living Trusts

A testamentary trust becomes effective upon your death and is usually established by your last will and testament. It enables you to control the distribution of your estate, including the opportunity to name a trustee for minor children’s assets, but does not avoid probate. You can change or revoke a testamentary trust during your lifetime.

A living trust takes effect during your lifetime. When you set up a living trust, you transfer the title of all the assets you wish to place in the trust from you as an individual to the trust. Technically, you no longer own the transferred assets. If you name yourself as trustee, you maintain full control of the assets and can buy, sell, or give them away as you see fit. However, this option may negate any estate tax benefits.

Living trusts can be revocable or irrevocable. A revocable trust can be dissolved or amended at any time while the grantor is still alive. An irrevocable trust, on the other hand, is generally difficult to modify or revoke.

Special-Purpose Trusts

Trusts, whether testamentary or living, can be established for a variety of specific purposes. Here are four of the most common.

Charitable trust — Enables you to provide a charitable organization with a regular income for a set period or a lump sum at the end of the period.

Incentive trust — Makes the transfer of assets to heirs contingent on their meeting goals or expectations, such as attaining higher education or starting a family.

Supplemental or special-needs trust — Can help provide for a disabled child and may ensure that the child continues to qualify for government assistance programs.

Life insurance trust — Can help ensure that the proceeds of a life insurance policy are excluded from your estate. (The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a life insurance strategy, it would be prudent to make sure that you are insurable.)

The use of trusts involves a complex web of tax rules and regulations, and there are costs associated with creating and maintaining a trust. Consider the counsel of an experienced estate planning professional and your legal and tax advisers before implementing a trust strategy.

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc.